Deposits pay less and less and mortgages will remain expensive for longer. Since the European Central Bank (ECB) lowered interest rates from 4.5% to 4.25% at the beginning of June, retail customers have wondered what will happen to the two banking products par excellence. And although the rate reduction is not excessive and not too much time has passed, the banks have already marked the line that will dominate the banking showcase, awaiting new macroeconomic signals.

In recent months, and before the ECB undertook the first interest rate cut, entities had already been adjusting their deposit supply downwards, anticipating a turn in monetary policy. Since interest rates are now higher than they will (expectedly) be in a few months, shorter durations offer the best returns. If half a year ago it was possible to find interest rates close to 4%, now the offer has fallen practically one point, to 3%.

On three-month deposits, Cetelem pays 4% APR and the Italian bank BFF 3.8%. But there have already been downward movements. MyInvestor has reduced its three-month deposit from 4% to 3.5%. And you must also keep in mind that the APR refers to annual interest, but these deposits only pay in three months. That is, the final remuneration that the client will receive in a three-month deposit is a quarter of what he would obtain if he maintained the balance for twelve months. To give an example, for a balance of 10,000 euros in a one-year deposit that pays 4%, at the end of the period the client would receive 400 euros gross. With that same balance, at the same interest rate, but with a duration of three months, the client would earn about 100 euros.

For longer durations, banks have already lowered profitability. The best deposit offers for six fall half a point to the 3.55% paid by BFF or 3.5% by Cetelem. At one year, the offer is even lower and barely exceeds 3%: Cetelem pays 3.2%, Pibank 3.14% and EBN and Banca March 3.1%.

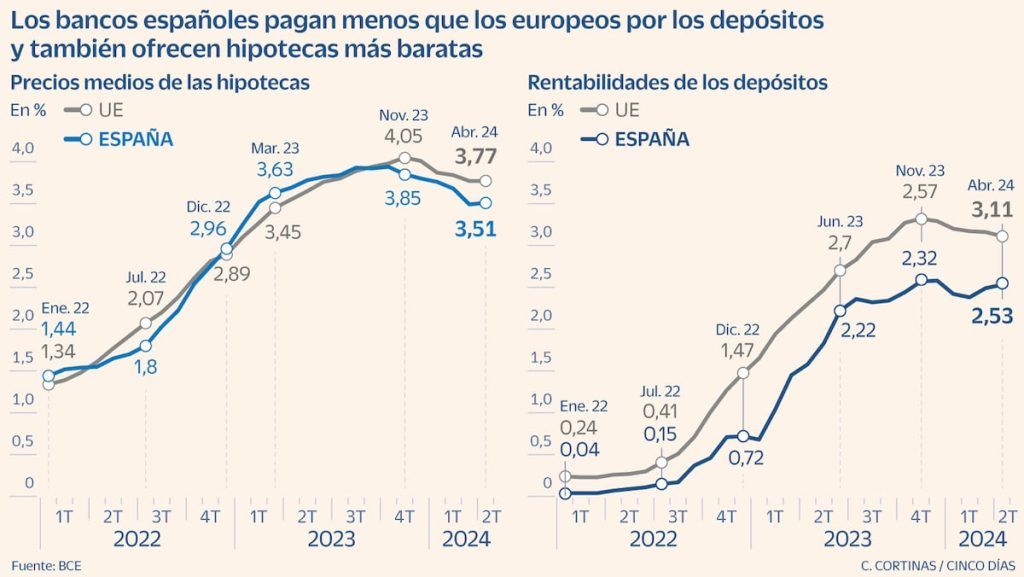

In reality, Spanish banks have remained behind Europe in terms of deposit remuneration over the last two years. In the month of April (which is the latest data available from the ECB), on average, national entities paid interest of 2.53% while the European Union average was 3.11%. Only banks in Croatia (1.81%), Greece (1.92%), Slovenia (1.85%) and Cyprus (2.06%) pay less than the Spanish ones. The sector has been justifying this little or no remuneration for liabilities in which they have excessive liquidity, due to the savings accumulated during the years of the pandemic by households and the ECB programs (known as TLTRO) that facilitated financing for banks.

In that sense, this week, the vice president of the European supervisor, Luis de Guindos, assured that deposits could be relaunched because entities no longer have so much excess money and those programs that facilitated financing have already ended. “This will lead, in our view, to more competition and to banks starting to compete more for deposits, including demand savings,” he declared. However, experts see little chance that deposits will increase.

“The banks’ balance sheets show that their main source of financing is customer deposits and current accounts and they must maintain a certain commercial incentive in rates for more stable financing. But the interest rates offered by Spanish financial entities have generally been lower compared to other countries, so significant movements in this regard are not to be expected to date,” explain Carlos Marcos and Breogán Porta, partners responsible for the sector. banking in Forvis Mazars.

In remunerated accounts, Trade Republic reduced the interest it pays on the accumulated balance from 4% to 3.75% on the same day that the ECB carried out the rate cut. Sabadell, before the change in monetary policy, paid 3% to new online account customers and once that promotion ended it launched another one, but which pays 2.5% APR.

Expensive mortgages for longer

After the interest rate cut, many clients with their sights set on purchasing a home expected a reduction in mortgage prices. However, they will have to wait even longer. As financial experts explain, interest on loans will remain high for longer. In that sense, they rule out an imminent mortgage war, regardless of whether any entity can make offers ad hoc for certain clients or adopt a more aggressive commercial policy to gain market share, as BBVA had been doing since the beginning of the year.

On the one hand, experts explain that banks were already anticipating a rate cut before the summer and in the first months of the year they had (slightly) lowered mortgage prices, so there will be no additional movements. To do this, they detail that entities need more clarity about the monetary policy path that the central bank will follow.

“The short-term effect is being minimal while waiting for the drop in inflation to settle and confirm and new rate cuts to come into view. The banks had already been discounting this drop in interest rates. They have been adapting their offer since the beginning of the year, offering mortgages below 4.25%. Added to this is that it is a small drop, of only 0.25 points, and that the prospects for when the next interest rate drop will occur are no longer clear,” they point out from the specialized finance platform Roams.

On the other hand, experts also detail that banks do not want to run the risk of entering into a war that overheats the mortgage market. Although inflation levels are more contained, banks still need macroeconomic signs of a recovery accompanied by additional declines to see lower prices on mortgage loans.

“The prices remain the same, there are only improvements for selected profiles. Many customers rely on banks to lower prices. But for that to happen, the ECB needs to lower rates further or give the market more signals of clarity. Until they see a clear path for monetary policy, banks are not going to take the risk of entering into a mortgage war and overheating the market,” says Marcelo Siqueira, director of operations at the mortgage broker Bayteca.

Regarding the type of loans, mixed mortgages continue to dominate the banking offer. According to Roams data, these loans have increased by 24% so far this year to the detriment of some variable mortgages that have begun to disappear from the catalog. “People have become afraid of the Euribor, which is causing this high demand for mixed mortgages. The fixed percentage is usually somewhat lower than that of fixed mortgages, so the client is guaranteed peace of mind with that fixed fee and when the time comes for the variable rate, it is decided based on how the market is at that time,” points out.

Just as Spanish banks have remained behind Europe in the returns they pay on deposits, they have also offered mortgages at lower rates than the rest of Europe. According to the latest data, the average mortgage in Spain is sold at a rate of 3.51% while the EU average is 3.77%. In general, large entities market rates that are around 4% (without taking into account possible bonuses when contracting other products). Among the current offer, Openbank (3.5%), EVO Banco (3.58%) and MyInvestor (3.7%) offer the lowest prices.

Follow all the information Five days in Facebook, x and Linkedinor in our newsletter Five Day Agenda

Newsletters

Sign up to receive exclusive economic information and the financial news most relevant to you

Sign up!

{kind=link}