Bloomberg— As optimism grows among investors in the face of the imminent US Treasury bond rally, a key indicator of the fixed income market emits a worrying signal for those thinking about investing.

First, the good news. With the midpoint of 2024 in sight, the Treasury bonds are about to erase their losses for the year, as signs finally emerge that inflation and the labor market are truly cooling. The Traders are now betting that this will be enough for the Federal Reserve to begin cutting interest rates as early as September.

But which could limit trimming ability of the central bank and, therefore, create a headwind for bondsis the increasingly widespread opinion in the markets that the so-called neutral type of the economy -a theoretical level of borrowing costs that neither stimulates nor slows growth- is much higher than policymakers currently anticipate.

“The meaning is that when the economy slows down inevitably, there will be fewer rate cuts and interest rates in the next ten years or so could be higher than they were in the last ten years”said Troy Ludtka, senior U.S. economist at SMBC Nikko Securities America, Inc.

The forward contracts referenced to the five-year interest rate in the next five years -an approximation of the market’s view on where US rates could end up- have stagnated at 3.6%. Although it is down from last year’s high of 4.5%, it is still more than a percentage higher than the average of the last decade and above the Federal Reserve’s own estimate of 2.75%.

This is important because means the market is pricing in a much higher floor for returns. The practical implication is that there are potential limits to how far bonuses can go. This should worry investors preparing for the kind of epic bond rally that bailed them out late last year.

The market’s neutral rate is higher than the Fed’s(Bloomberg)

For now, Investor mood is increasingly optimistic. A Bloomberg gauge of Treasury yields was down just 0.3% in 2024 as of Friday, after losing as much as 3.4% for the year at its lowest point. Benchmark yields are down about half a percentage point from their year-to-date high in April.

In the last sessions, the Traders have turned to contrarian bets that benefit from increased odds that the Federal Reserve will cut interest rates as soon as July.and the demand for futures contracts that point to a rebound in the bond market.

But If the market is right that the neutral rate -which cannot be observed in real time because it is subject to too many forces- has risen permanently, then the current Fed reference rate, above 5%, may not be as restrictive as perceived. In fact, a Bloomberg indicator suggests that financial conditions are relatively easy.

“We’ve only seen a fairly gradual slowdown in economic growth, and that would suggest that the neutral rate is significantly higher,” said Bob Elliott, CEO and Chief Investment Officer of Unlimited Funds Inc. With the current economic conditions and the limited risk premiums of long-term bonds, “cash seems more attractive than bonds”he added.

The true level of the neutral type, or R-Staras it is also known, has become the subject of heated debate. Reasons for a possible upward shift, which would mark a reversal of the decades-long downward trend, include expectations of large and prolonged public budget deficits and increased investment to fight climate change.

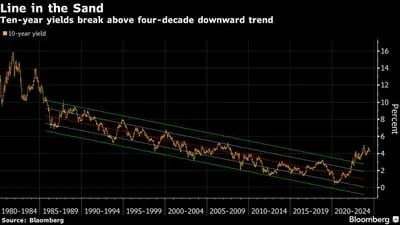

Ten-year yields break four-decade downtrend(Bloomberg)

A more pronounced slowdown in inflation may be necessary for bonds to continue rising and growth that leads to faster and deeper interest rate cuts than the Federal Reserve currently anticipates. A higher neutral rate would make this scenario less likely.

The economists hope that next week’s data show that the Fed’s preferred gauge of core inflation slowed to an annualized rate of 2.6% last month from 2.8%. Although this is the lowest reading since March 2021, remains above the Fed’s target of 2% inflation. And the unemployment rate has been at or below 4% for more than two years, the best performance since the 1960s.

“While we see pockets of households and businesses suffering from higher rates, overall, as a system, we have clearly handled this very well,” said Phoebe White, head of U.S. inflation strategy at JPMorgan Chase & Co. .

He Financial market behavior also suggests that Fed policy may not be restrictive enough. The S&P 500 has broken records almost daily, even as inflation-adjusted rates with shorter maturities, cited by Fed Chair Jerome Powell as a gauge to gauge the impact of Fed policy, have risen almost 6 percentage points from 2022.

“You have a market that has been incredibly resilient in the face of higher real yields,” said Jerome Schneider, head of short-term portfolio management and financing at Pacific Investment Management Co.

What Bloomberg Strategists Say

“In the space of just a couple of points, the Federal Reserve has raised its estimate of the nominal neutral rate from 2.50% to 2.80% – showing how central banks around the world are still trying to get its arms around the scale of economic expansion and inflation seen in this cycle. That’s why, current market assessment, which expects almost two full rate cuts from the Fed this year, seems overstated”.

– Ven Ram, cross-asset strategist.

With the exception of some Federal Reserve officials, such as Governor Christopher Waller, most policymakers lean toward higher neutral rates. But their estimates varied widely between 2.4% and 3.75%, underscoring the uncertainties in making the forecasts.

Powell, speaking with reporters on June 12 after the central bank’s two-day policy meeting adjourned, appeared to play down its importance in the Fed’s decision-making, stating that “we can’t really know” whether neutral rates have increased or not.

For some in the market, it is not an unknown. It is a new higher reality. And it’s a potential roadblock to a rally.

What to pay attention to:

Economic data:

- June 24: Dallas Fed manufacturing activity.

- June 25: Philadelphia Fed non-manufacturing activity; Chicago Fed domestic activity; FHFA Home Price Index; S&P CoreLogic; Conference Board Consumer Confidence; Richmond Fed manufacturing and business conditions index; Dallas Fed services activity.

- June 26: MBA Mortgage Applications; sale of new homes.

- June 27: Goods trade balance advanced; Q1 GDP (third reading); wholesale/retail inventories; initial unemployment benefit claims; durable goods; pending home sales; Kansas City Fed manufacturing.

- June 28: Personal income and expenses; PCE deflator; Chicago PMI MNI; sentiment from the University of Michigan (final reading); Kansas City Fed services.

Fed Calendar:

- June 24: Fed Governor Christopher Waller; San Francisco Fed President Mary Daly.

- June 25: Michelle Bowman, Fed Governor; Lisa Cook, Governor of the Fed.

- June 28: Thomas Barkin, president of the Richmond Fed; Bowman.

Auction calendar:

- June 24: letters at 13 and 26 weeks.

- June 25: CMB at 42 days; 2-year promissory notes.

- June 26: 2-year FRN reopened; letters at 17 weeks; 5-year promissory notes.

- June 27: letters at 4, 8 weeks; 7-year promissory notes.

Read more at Blommberg.com

{kind=link}