This column was written by guest columnist Jorge Llano.

The Congress of the Republic is debating a pension reform that is dramatically different from the expected objectives of a pension system: more coverage, an equitable and sustainable system, for today and future generations.

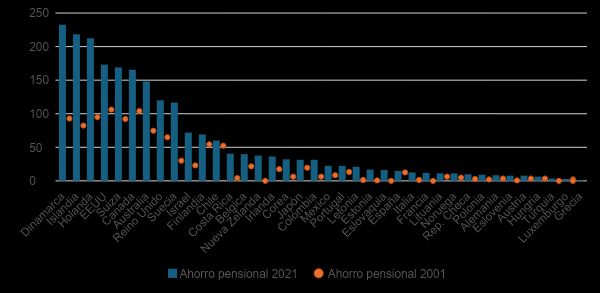

All countries face these challenges and, given this, the vast majority of countries in the Organization for Economic Cooperation and Development (OECD) have chosen to introduce components of the pension system based on savings, since it is an inexorable truth that a system that does not save It is a system that makes water in the future. As we can see in the following graph, the growth of pension savings as a percentage of the Gross Domestic Product (GDP) for most countries, including Colombia, has been constant. Several countries have pension savings above 100% of GDP.

Pension savings as a % of GDP.

Overcoming the discussion on the optimal level of pension savings, and always seeking a high amount to provide more and better pensions, the discussion on its administration continues. Some countries have opted for an administration independent of the government, but carried out by public entities, such as the Canadian case, others have relied on private managers, such as Denmark and the Netherlands.

In the Colombian case, I am convinced that the best balance would have been for the public sector to compete on equal terms with private managers, that is, the creation of a public AFP, but to manage the resources under the same supervision and rules of the game as the Private AFPs.

However, in Colombia it seems that we are doing things the other way around, since today a reform is being voted on that reduces pension savings into the future, as a percentage of GDP, and makes its entire sustainability depend on having a dependency rate for older adults. low. Quite the opposite is what we know will happen given the demographic transition.

With these figures we can already predict that we will have an important macroeconomic impact, since we are a country that saves little (about 14% of GDP in annual terms) and with this we will save even less. This is a vicious circle: lower savings translate into a negative effect on the capital market, lower investment, lower potential GDP, and lower future economic growth.

Worsening the level of pension savings, the discussion has cited who will manage part of that lower savings, which will last until 2070 at most.

As it is necessary to create rules of the game so that the negative effects are not even stronger, the discussion raised these days is about the administration of part of that pension savings that the reform will leave us. The options are very limited.

On the one hand, the government initially proposed something very similar to what we have today with the National Pension Fund of Territorial Entities (Fonpet) where the administration rests in the Ministry of Finance and those resources are put out to tender to entities with experience. in the management of that type of assets.

On the other hand, it has been proposed that the Bank of the Republic be the entity in charge of managing these resources, and the Bank could also put out to tender the management of that money.

Fonpet is a success story for its creation, but not for the administration of resources. As studied by the AMV, it is observed that the Fonpet bidding process has not led to a portfolio managed with a long-term vision and that its diversification is very low. We see that today no private entities came forward to manage that money and it is the Public Credit Directorate that has those resources in its coffers, without being correctly invested.

A new Fonpet would seem to be the best possible scenario in case it is decided that the government manages these resources. Given this, I share the proposal that the Bank of the Republic be the one to assume that responsibility.

The reasons for this are: the independence of this entity, which has been tested multiple times, even when the presidents have been able to have, at least on paper, a majority on their board. Additionally, it is a technical entity that already manages pension liabilities, as it has its own autonomous assets for Bank pensioners. It has also managed public funds such as the Reserve Fund for the Stabilization of the Mortgage Portfolio (Frech) and manages nearly 60 billion dollars of international reserves.

Regarding the criticisms, all very valid, some reflections. The Board of Directors of the Bank should not be the same Board of Directors of the Savings Fund, since the skills required of one and the other are not necessarily the same. Now, this Council must be appointed by the Board of the Bank and if it has a representative of the government in power, it should be, at most, one.

Regarding the conflict of interest, I believe it is limited, since interest rate movements respond to short-term deviations. This period is not material in the administration of pension resources, while the longer-term objective, which is macroeconomic stability, especially of prices, is fully aligned with the period with which these resources are being administered.

And finally, regarding the criticism of the possible reputational risk, it is worth asking ourselves two things: first, how many times have Fonpet’s returns been publicly analyzed? They are more comparable to this fund created by the reform and less to the AFPs. , since the amount of the pensions will not depend on the profitability of said investments.

And second, isn’t it precisely an achievement of the Bank that, by doing an unpopular job like managing the intervention interest rate, today it has such high credibility in the general population?

It is clear that we are discussing a lesser evil. I am delighted to hear other proposals to try to mitigate the negative effects of the reform, but always with the hope that in the coming years we will be able to straighten the path, and create the foundations for a reform that does think about future generations.

The opinions I express here do not involve the place where I work.

Jorge Llano

Vice President of Market Development. Economist and master’s degree in Economics from the Universidad de los Andes, with a master’s degree in Public Administration from Columbia University (New York). He was a consultant at the National Planning Department and advisor to the Ministry of Finance. He also worked at Asofondos.

{kind=link}